Disclaimer: This is not financial advice. I just work in the Medicare industry and thought I would share some knowledge. I have no affiliation with any of the companies mentioned in this post. I do own shares in some of the securities discussed.

//

There are two keys to success in the Medicare market:

Membership growth is fairly straightforward to understand. You need to grow membership in order to grow the monthly recurring revenue received from Medicare. Star ratings are a little more complicated but equally important.

//

Background on Medicare Star Ratings

Medicare uses a star rating system to rate the performance of every Medicare Advantage (MA) plan each year. They created the system to prevent MA plans from cutting costs and maximizing profits at the expense of the member. Some examples include denying reimbursement or reducing customer service staff in the pursuit of higher profit margins. The star rating system prevents this.

MA plans care about star ratings because it has a huge impact on their top and bottom line each year. A higher star rating directly improves enrollment rates, revenue growth, and profitability.

The MA plans get rated on a scale of 1 (worst) to 5 (best). 3-star is average. Below 3-star is poor, and if a plan remains below 3-star for multiple years in a row they can actually lose their contract with Medicare. New plans are fixed at 3.5 stars for the first few years in order to give them time to implement performance-improvement efforts and generate data.

4-star is good, and each year that a plan gets a 4+ star rating they end up getting a $500 bonus per member. That directly increases their top line revenue by 5% and represents pure profit. They already incurred all their expenses for the year, so the bonus payment after the year ends drops directly to the bottom line. With an average profit margin of 5% across the industry, the 4+ star bonus payment effectively represents all the profits of the industry.

The other benefit of star ratings is improved enrollment rates. Star ratings are published online for Medicare beneficiaries to see. People typically choose to enroll in higher-rated plans. In fact, each 0.5-star improvement is correlated with 6% higher enrollment rates.

//

CLOV Star Rating

CLOV is currently a 3-star plan for 2021. This is partly the reason they are not yet profitable (along with the expenses associated with high growth).

There are three reasons why CLOV is only a 3-star plan:

- CLOV is a startup launching new plans each year, and most new plans are below 4 stars. The average star rating for new plans is 3.48. Bright Health (BHG) is a highly-valued peer that went public in 2021, and they are a 2.5-star plan. It takes time to establish relationships with providers and collect data on members that can be used to improve outcomes and star ratings.

- CLOV offers PPO plans, which is why people choose them. PPO plans offer more flexibility, allowing members to stay with their current provider. This means CLOV has to work with a wider network of providers, which makes it more difficult to impact outcomes. HMO plans have narrow networks, often forcing people to switch to a specific provider in-network. This makes it easier for the MA plan to work closely with the provider and improve outcomes. Alignment Healthcare (ALHC) is a peer that went public in 2021, and they are a 4.5-star plan. They operate HMOs in California, which is a unique market where providers and patients are used to narrow networks. PPOs are not common.

- Star ratings are based on data from 1–2 years ago. At the end of each year, Medicare starts collecting data from all the MA plans and providers. This takes a while, and they don’t end up publishing the new star ratings until October of each year just in time for open enrollment. So for 2021 star ratings, the data is from 2019. The Clover Assistant was still nascent at that time, and they didn’t launch the key features designed for improving star ratings until the second half of 2019.

The Clover Assistant will be a key driver of star ratings for CLOV going forward. It’s designed to support providers in a way that helps them make the right decision to close gaps in care and improve outcomes. The Clover Assistant will be key for improving outcomes and reducing cost in Direct Contracting (DC) as well, which is why CLOV is investing so much into it.

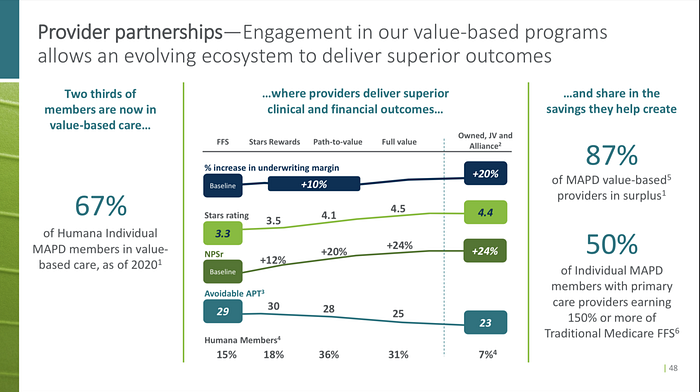

Below you can see the impact of MA plans closely collaborating with providers to improve star ratings. Traditional incumbents like Humana (HUM) and UnitedHealth (UNH) do this by acquiring providers or at least sharing risk with them. The Clover Assistant takes this relationship to the next level, providing insights and recommendations that the provider can act on.

//

CLOV 4+ Star Rating Timeline

CLOV needs to improve to 4+ stars over time in order to be a successful (i.e. profitable) MA plan. The most important market to watch is their anchor markets in New Jersey. That’s because new plans don’t get rated until year 3 (so all of CLOV’s new markets won’t have star ratings for a while). New Jersey is also where their most mature provider network is located, and where Clover Assistant will have the most immediate impact due to higher adoption rates.

I’m confident 4+ stars will be achieved in New Jersey by 2024, maybe 2023, but probably not 2022. Here’s why:

2022 Star Rating

Medicare is going to use 2019 data for many 2022 star measures due to a lack of data collection during the 2020 COVID outbreaks. For example, the diabetes glucose control measure requires members to go in for a doctor visit to get a blood test. Not many members did that in 2020. Since many measures will utilize the same data as previous star ratings, it’s likely that CLOV will remain a 3-star plan in 2022. When 2022 star ratings are announced this October, the market doesn’t expect an improvement.

2023 Star Rating

This year will be interesting because Medicare will finally have all the data they need to calculate fresh star ratings again. However, the data will still be heavily influenced by COVID. Geographies that were more impacted by COVID (i.e. NY/NJ) will likely have worse results than the national average. For example, since many diabetics did not see their doctor in 2020, their condition is likely to be uncontrolled in 2021 when they get their blood results. This will have a negative impact on star measures. I expect Medicare will come up with some normalization method to help mitigate the geographic impact of COVID on the 2023 star ratings.

2023 could be the first year CLOV ends up achieving a 4+ overall star rating. If they do, it will be driven by the member experience star measures. Member experience measures currently have double-weighting for 2021. Medicare is increasing their weighting starting in 2023 to quadruple weighting, at which point they will represent 46% of a plans overall star rating. CLOV scored 4+ on 7 out of 9 member experience measures for 2021. That’s a strong sign that the re-weighting of member experience measures will naturally boost CLOV’s overall star rating starting in 2023. The 2023 star ratings will be announced in October of next year, which could be a big catalyst. If CLOV achieves 4 stars, I would expect the stock to have a huge rally.

2024 Star Rating

2024 star ratings will be the first true look at CLOV’s performance since launching Clover Assistant features in the second half of 2019. 2024 star ratings will be based on 2022 performance, so the up-and-down impact of COVID on claims and data collection should finally be over. These ratings will be announced in October of 2023. This could be the ultimate catalyst because it will finally show the impact of Clover Assistant on health outcomes, star ratings, and profitability. The value of Clover Assistant will also be extrapolated across all of CLOV’s members and markets at that point, which should be 140,000+ MA members and 400+ MA markets at their current growth rate. The value of the Clover Assistant also applies to DC members, where profits and losses are based on health outcomes and controlling costs.

//

Summary

CLOV is in an interesting position these next 12 months. Most of their plans (i.e. market-level contracts) are new, which means they won’t receive a star rating for a couple of years. COVID has also resulted in their mature plans being fixed at 3-stars for a couple of years.

In the interim, CLOV may report on some key performance indicators (KPI) that could provide some guidance on the performance of the Clover Assistant, even if star ratings won’t be impacted in the short-term:

- Clover Assistant adoption (contracts with providers). This will be a leading indicator of Clover Assistant’s potential impact across markets, and the maturity of the provider network, which both affect outcomes and star ratings.

- Clover Assistant usage (within provider contracts in mature markets). This will be a leading indicator of the potential impact of Clover Assistant at the provider-level within each market.

- Clover Assistant results (outcomes and quality measures compared to providers not using Clover Assistant). This will be a leading indicator of star ratings and profitability in future years within each mature market that Clover Assistant is deployed.

Fixed star ratings through 2022 may turn out to be a blessing for CLOV long-term. It allows them to continue developing, refining, and improving the Clover Assistant based on provider feedback and patient outcomes. It also allows them to run bold experiments that may or may not work, without getting penalized by Medicare or the market. This will position them for a stronger performance going into 2023 with a more robust software platform, valuable learnings, and tighter provider partnerships. If all this translates into a 4+ star rating, CLOV shareholders will be generously rewarded.

Until then, it’s all about growth metrics. The higher the growth achieved, the larger the bonus since it’s based on the number of members. Riding CLOV up the growth curve and holding through 2023 should be a formula for success.