Retail investors are changing markets forever. But what comes after a short squeeze? It could be huge growth for CLOV.

Disclaimer: This is not financial advice. I just work in the Medicare industry and thought I would share some knowledge. I have no affiliation with any of the companies mentioned in this post. I do own shares in some of the securities discussed.

//

On March 6th, 2009, President Obama was newly sworn in and his first order of business was to stabilize the American economy after the finance industry almost destroyed it. People all over the world had lost much of their life savings because of Wall Street’s greed.

After stimulus passed, the administration started to work on their next major legislative policy.

It was healthcare.

//

On that same day in 2009, UnitedHealth (UNH) was trading at $17.90 with a market cap of $16.9B.

On that same day in 2009, Humana (HUM) was trading at $19.54 with a market cap of $2.5B.

Industry valuations were compressed due to the legislative risk that could be coming from the Obama administration. It turns out legislation would be a positive catalyst for the industry.

The Obama administration ended up passing the Affordable Care Act (ACA) on March 23rd, 2010. The ACA has dramatically changed the US healthcare system. Now that it’s survived both Democratic and Republican administrations, it will continue to spark more change long-term. The ACA gives Medicare the power to change payment models in a way that moves the entire industry away from “fee-for-service” (FFS) to “value-based care”. It does this by giving the private sector huge financial incentives to improve outcomes.

Since early 2009, UnitedHealth (UNH) and Humana (HUM) have grown over 23x. The Medicare market is what has primarily driven the industry’s growth. UNH is the largest Medicare Advantage (MA) insurer in the US, with 26% market share. HUM is close behind them. Much of the growth of these large insurers have been through the acquisition of MA plans in local markets all over the country.

CLOV isn’t a short-term meme stock. It’s a long-term dream stock.

23x growth is the opportunity Clover Health (CLOV) has AFTER a short squeeze. It’s one of the most heavily shorted stocks in the market. With the support of retail investors, they can use their elevated stock price as an asset to invest in growth and go on a series of acquisitions that create real business value. This growth will support an even higher stock price. It’s a virtuous cycle.

Healthcare providers and insurers have stable revenue streams, making it straightforward to finance their acquisition. UNH and HUM have already proven this playbook over the past 10 years. It’s right in front of us. CLOV can replicate it, and with a strong retail backing, they can execute this same playbook in an even shorter time period. The retail revolution has arrived at the exact same time that there is massive disruption (i.e. opportunity) in the healthcare industry.

Retail investors now have the power to create long-term winners, not just beat short sellers.

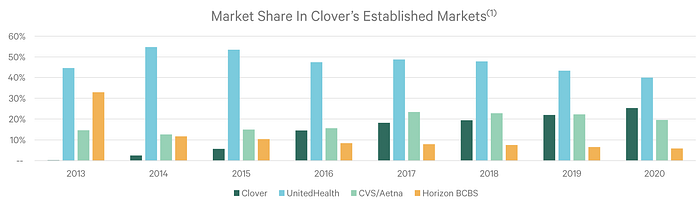

CLOV is perfectly positioned to replicate the UNH and HUM playbook and beat them at their own game. CLOV has run Medicare Advantage (MA) plans for over seven years. They’ve been able to take more and more market share away from UNH and other large competitors each year. That’s made them one of the fastest-growing MA plans. The most amazing part is that it’s been entirely organic growth.

With more retail investors, they can rapidly launch and/or acquire new MA plans in geographies that they’re not currently in. They also have the Clover Assistant, a software platform that providers use to improve health outcomes. With their Direct Contracting Entity (DCE), CLOV can collaborate with provider organizations around the country and take on full-risk with them using the Clover Assistant. They could rapidly become one of the largest Payvidors in the US.

The future of US healthcare will be dominated by Payvidors. It’s a combination of a payor (i.e. insurance company) and provider (i.e. doctor). It’s powerful because you can take on and manage risk as a payor, and directly control cost and quality on the provider side. Kaiser Permanente has proven out this model in the US for decades now. UNH has become the ultimate example of a Payvidor, growing from an insurer 10 years ago to the largest employer of physicians in the US.

This is the next stage of evolution in the retail revolution.

GME and AMC have been amazing stories so far. They’ve given retail a voice that Wall Street can’t ignore. Nothing changed after 2008. Now they’re being forced to change through the transparency that retail investors are demanding. As the retail investor movement grows, I hope we can also support companies that are positioned for future growth, like CLOV.

If we could do that, we might just take control of this entire game.

//

Note:

This thesis isn’t specific to CLOV or healthcare. I truly believe retail investors can create massive value for all companies and industries positioned for growth. I just know healthcare, and see a proven model that can be replicated by a great company that also happens to be highly shorted.