Value-Based Care: The evolution of Clover Health into a Payvidor.

Disclaimer: This is not financial advice. I just work in the Medicare industry and thought I would share some knowledge. I have no affiliation with any of the companies mentioned in this post. I do own shares in some of the securities discussed.

Value-based care (VBC) refers to the payment of healthcare providers based on performance. Traditionally, providers have been paid based on fee-for-service (FFS). This has led to higher and higher volumes and cost, which is why Medicare is executing a long-term roadmap to shift the entire US healthcare system to value-based payment models.

The focus of VBC payment models is primary care physicians (PCP). That’s because PCPs control the flow of the patient through the healthcare system. When you need a check-up or you don’t feel well, you’re going to see a PCP. Therefore they control the overall cost of a patient ($10,000 per year for a Medicare patient). Paradoxically, PCPs are the lowest-paid specialty in the US and account for only 5% of overall healthcare spending in traditional FFS payment models. The average PCP visit costs $121.45.

In VBC payment models, they’re the most important specialty and the point at which performance is measured and payment is delivered. VBC providers are primary care groups that take on risk with a payor to be responsible for the overall cost of the patient. The payor could either be the government (Medicare) or a private health plan (Medicare Advantage). In these models, the PCP goes from receiving $100 per visit to receiving up to $10,000 per patient per year to manage.

That’s why value-based care is such a huge opportunity.

//

Value-based care landscape.

There are different business models to delivering primary care. The two most important dimensions to consider when looking at a value-based care provider is their care model and their operating model. The care model could be brick-and-mortar clinics, home visits, virtual care, or a combination of all three. The operating model could be a traditional medical group that owns and operates clinics, a partnership structure that contracts with independent primary care practices, or a hybrid of the two. The operating model determines the flow of money and unit economics.

Traditional Model

Clinics owned and operated by a central risk-bearing medical group that employs all the clinicians and staff. The medical group holds the contract with Medicare (Direct Contracting) and Medicare Advantage plans.

- Cano Health (CANO): 72 practices in 3 states and Puerto Rico(source)

- Oak Street Health (OSH): 54 practices in 8 states (source).

- ChenMed (Private): 75 practices in 10 states (source)

- Iora Health (Private): 48 practices in 10 states (source)

Partnership Model

Management Service Organizations (MSO) aggregate existing primary care practices into a network of providers that take on risk together through contracts held by the MSO. The individual providers maintain ownership over their practice and employ their own staff, but are paid by the MSO through risk-based agreements.

- Apollo Medical (AMEH): 7,000 partner primary care providers (source)

- Agilon Health (AGL): Number of partner providers undisclosed (source)

- Aledade (Private): 550 partner primary care practices (source)

Hybrid Model

- VillageMD (Private): 2,900 employed or partner primary care providers (source)

- Privia Health (Private): 2,500 employed or partner primary care providers (source)

//

CLOV in value-based care.

CLOV has traditionally been a payor (Medicare Advantage plan). They’re now entering into the value-based care landscape in multiple ways to become a combination of a payor and provider (‘Payvidor’). Payvidors are the future of US healthcare because they can take on and manage risk as a payor, and directly control cost and quality on the provider side. It’s a proven model that continues to show success.

CLOV is stepping into value-based care was with the Direct Contracting (DC) program. Like some of the value-based care providers above, CLOV is one of 53 organizations approved as a Direct Contracting Entity (DCE). The DC program just started in April 2021, and so far CLOV has the highest publicly-announced enrollment in the country. DCE’s take on risk directly with Medicare, and then contract with a network of providers who share that risk (i.e.‘Partnership Model’ above). As part of the DCE, the providers collaborate closely with CLOV to control quality and cost.

Another way CLOV is working in value-based care is through Clover Home Care, it’s in-home primary care service (i.e. home visits). Home care hasn’t been possible in fee-for-service payment models because $100 won’t cover the cost of traveling to the patient’s home. In value-based care, providers are not paid per visit, so it doesn’t matter if you’re seeing the patient in the clinic, at home, or through a video call.

Brick-and-mortar clinics could become far less valuable in the future. Payvidors could manage populations more efficiently without any physical footprint. They could send a medical assistant to the home to take the patient’s vitals and have the doctor join via televisit. Home visits could be more effective too, because the clinician can observe the home environment, address any fall risks, identify social needs, etc. The convenience of home visits can also lead to higher enrollment into CLOV’s Medicare Advantage plans or DCE.

//

CLOV as a Payvidor

CLOV’s Medicare Advantage plans are a great business. It’s a recurring revenue business model with high growth rates. However, there’s a limit to how much of the Medicare premium they can legally keep (15%). This is effectively a cap on profit margins, which is why the average Medicare Advantage plan reports a 5% margin after SG&A costs. In Direct Contracting, there’s no limit to how much you can keep. It’s 100% shared savings, so the more costs you save, the more money you make. Typically providers target 15% operating margins in risk-based contracts, which is 3x higher than the average 5% margin for Medicare Advantage plans.

By partnering with providers, they can reduce overall costs and keep more of the DC premium. And by delivering home care services, they can directly improve outcomes for the most complex and costly patients. Altogether, the Payvidor model will generate higher growth and better unit economics for CLOV.

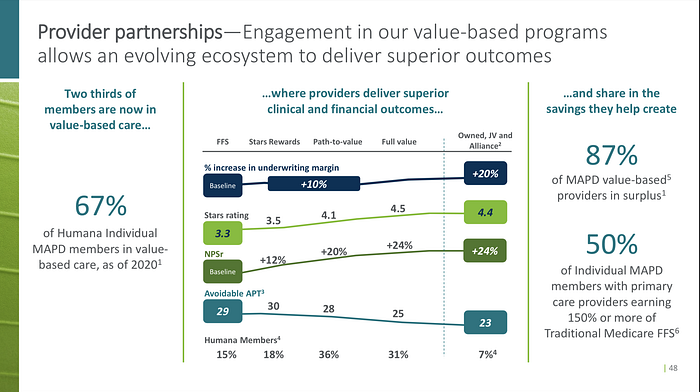

Medicare Advantage competitors like UnitedHealth (UNH) and Humana (HUM) are becoming Payvidors by acquiring provider groups. This is an expensive and time-consuming strategy, which indicates how important the provider is to succeed in the Medicare market. Below you can see the direct impact provider partnerships have on Medicare Advantage performance (i.e. star ratings and operating margins), especially when the MA plan shares risk with the provider partners:

If CLOV can use the Clover Assistant to achieve a 4-star rating with providers in their PPO network, then they officially achieved the holy grail. They don’t need to spend significant resources acquiring providers through exclusive partnerships, investments, or acquisitions. They can offer more flexible PPO plans that drive higher enrollment and member satisfaction compared to narrow-network HMO plans that force the member to switch providers.

They essentially become a virtual Payvidor, achieving the same results as the leading incumbents with a fraction of the capital and timelines required. This would be a true disruption to the industry.